The vast majority of problems, conflicts and stress we see in the closing process are with closings that are scheduled on Fridays or the last three days of the month.

That is true all year but is especially true in the spring and summer when the real estate business in our market is busiest.

2021’s busy season started early, so everyone needs to make sure when putting dates and expectations in their contracts, they plan for success by avoiding those problem days.

Everything works back from the closing date, and for a lot of reasons, people like to close on those no-go days. As a result, lenders, surveyors, home inspectors – all your partners in your real estate business – are trying to work through an uneven pipeline demand. This creates bottlenecks; bottlenecks cause unexpected delays and last-minute surprises no one wants.

You can help them, your customers, and yourself by trying to schedule mid-week closings and closings near the 10th and 20th of the month. There will be fewer opportunities for delay, and a better chance for that smooth and successful real estate experience that generates years of referral business for you.

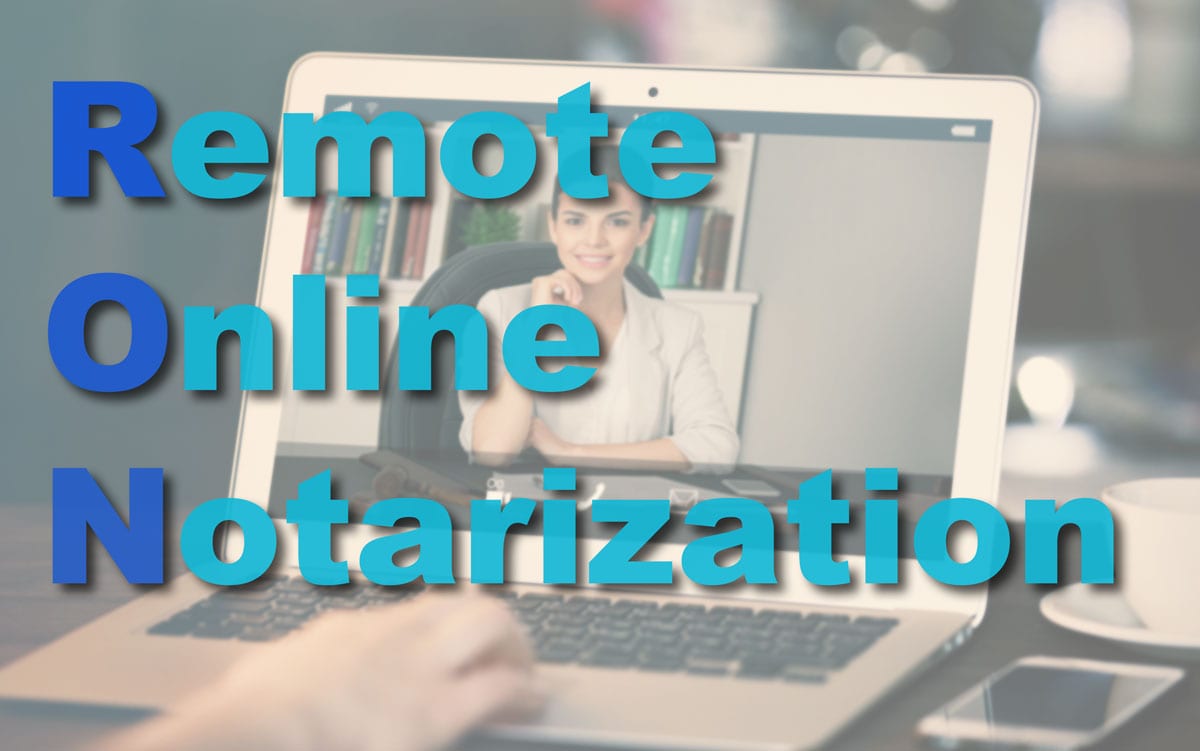

With the New Year, Florida’s new Remote Online Notarization (RON) law is going into effect. This is the next step along the path toward e-closings.

With the New Year, Florida’s new Remote Online Notarization (RON) law is going into effect. This is the next step along the path toward e-closings. Are you working with a buyer who is looking at purchasing a HUD owned property?

Are you working with a buyer who is looking at purchasing a HUD owned property?